Mostrando postagens com marcador recessão. Mostrar todas as postagens

Mostrando postagens com marcador recessão. Mostrar todas as postagens

07 setembro 2014

Frase

16 junho 2014

Não conhecemos a causa de inflação ou recessões

Macroeconomics is a little like fusion power. When the Great Depression hit, economists finally started taking booms and busts seriously. There’s no denying that something weird happens when a country slips into recession -- all the same factories and offices and people and ideas are there, but suddenly people aren’t producing as much stuff. Why? John Maynard Keynes, Friedrich Hayek and Irving Fisher wrestled with this question in the 1930s, and their work kicked off a decades-long quest to understand what we now call the business cycle. But almost a century later, despite sending some of our best brains up against the problem, we’ve made frustratingly little progress.

It’s hard to overstate how few solid conclusions have emerged out of a century of macroeconomic research. We don’t even have a good grasp of what causes recessions. Robert Lucas, probably the most influential macroeconomist since Keynes, had this to say in 2012:

I was [initially] convinced…that all depressions are mainly monetary in origin…I now believe that the evidence on post-war recessions (up to but not including the one we are now in) overwhelmingly supports the dominant importance of real shocks. But I remain convinced of the importance of financial shocks in the 1930s and the years after 2008. Of course, this means I have to renounce the view that business cycles are all alike!

Lucas’ progression roughly reflects the shifting fads in academia. In the 1970s, people mostly thought that recessions were caused by tight monetary policy. After the big inflation in the '80s, people built models in which recessions happen because fewer new technologies got discovered in a given year. But that didn’t seem to explain the recessions induced by Federal Reserve Chairman Paul Volcker in the early 1980s, so new models were developed that attributed recessions, again, to tight monetary policy. After the financial crisis of 2008 and the deep recession that followed, macroeconomists shifted gears and started building models in which financial crises cause economic busts. The consensus shifts every time something big happens.

Other top macroeconomists put the problem even more starkly. Harvard’s Greg Mankiw said this in 2011:

After more than a quarter-century as a professional economist, I have a confession to make: There is a lot I don’t know about the economy. Indeed, the area of economics where I have devoted most of my energy and attention — the ups and downs of the business cycle — is where I find myself most often confronting important questions without obvious answers...

And in that same year, the University of Chicago’s John Cochranewrote:

Why are we stagnating? I don’t know. I don’t think anyone knows, really...Nothing on the conventional macro policy agenda reflects a clue why we’re stagnating...

We also don’t understand what causes inflation. It makes sense that printing more money would cause prices to rise, but trillions of dollars of quantitative easing -- a policy dreamed up by Milton Friedman as a way to fight stagnation -- haven’t budged the inflation rate from its low level of about 2 percent. That has led a small but growing number of macroeconomists, including Stephen Williamson of Washington University, to suggest that quantitative easing, or long periods of low interest rates, actually reduce inflation. At a recent Hoover Institute conference, Cochrane declared that inflation is actually the result, not of loose monetary policy, but of government borrowing (this is actually an old idea as well).

On the topic of what to do about recessions, opinion also is split. The dominant school of thought among macroeconomists (the “New Keynesians” and “monetarists”) says that fighting recessions is the Fed’s job -- lowering interest rates, or QE, or nominal gross domestic product targeting can get the job done. A branch of this school thinks that monetary policy loses its punch when interest rates are low, and recommends fiscal stimulus spending to fill the gap. A slightly smaller group (the “New Classicals”) think that nothing can be done -- we just need to wait it out, and in the meantime try to cut taxes and implement other structural reforms. The debate rages on. But this argument is a little like medieval doctors arguing over leeches versus bleeding -- without a real understanding of what causes recessions, our medicines are largely a shot in the dark.

Why is macroeconomics one of the great unsolved problems in the history of human science? It isn't because macroeconomists aren’t smart enough, as anyone who has hung around them knows. It’s also not because they’re too politicized; you can find macroeconomists on every end of the spectrum. Nor is it for lack of resources being thrown at the question.

The problem is data. Business cycles are few and far between. And business cycles that look similar to one another -- the Great Depression and the Great Recession, for example -- are even farther apart. It’s hard to tell whether policies have any effect, or whether those effects were about to happen anyway. The main statistical technique we have to analyze macro data -- time-series econometrics -- is notoriously inconclusive and unreliable, especially with so few data points. Comparing across countries helps a bit, but countries are all very different, and recessions can also spill over from one to another.

The uncomfortable truth is this: The reason we don’t really know why recessions happen, or how to fight them, is that we don’t have the tools to study them properly. This is the situation biologists were in when they were trying to fight disease before they had microscopes. Not only did they not have the right tools, they didn’t even have any way of knowing what the right tools would be!

So I can’t tell you when macroeconomics will have a real breakthrough. Will we be able to get insight from simulated economies (called agent-based models)? Will huge multiplayer online video games give us a laboratory to study recessions? Should we look at cities as economies, and gain some insight there? Or is there some other data-gathering method so different from what we do now that I can’t even imagine it?

It’s easy to point and laugh and say that macroeconomics isn’t a science. It’s also easy to convince yourself that if macroeconomists just ditched their blinkered political ideologies, all would become clear. But those are comforting fantasies. The fact is, there are just some big problems that mankind doesn’t know how to solve yet.

Fonte: aqui

16 julho 2013

Sentimento e Recessão

Os pesquisadores já sabem que os períodos de recessão geralmente são acompanhados por uma onda de pessimismo. Mas existe uma grande dificuldade de medir o pessimismo das pessoas, sendo geralmente usadas aproximações.

Na área de finanças comportamentais tem-se estudado como os sentidos influenciam as decisões financeiras. Pesquisas já comprovaram que o mercado acionário é influenciado pelo tempo, pelos resultados dos esportes, pela superstição, pelas notícias da imprensa, entre outras situações.

Diego Garcia, um pesquisador da Universidade da Carolina do Norte, resolveu investigar o papel da imprensa e o comportamento do mercado acionário. Para isto, ele usou uma de mais de cinquenta mil artigos que foram publicados diariamente no New York Times e Wall Street Journal, desde 1905 até 2005, sobre o mercado financeiro. Analisando cada um destes textos, Garcia classificou as palavras negativas (irregular, declínio, perda, destruição, etc) e positivas. Ao confrontar a quantidade de palavras de cada um dos grupos, para cada texto analisado, Garcia elaborou um índice de pessimismo do texto. De uma maneira geral, ele encontrou que os textos dos jornais são pessimistas, já que o número de palavras otimistas é menor que as negativas.

Além disto, ele comparou o índice, que representaria uma aproximação do sentimento do mercado ao longo do tempo, com o comportamento do próprio mercado. E encontrou que o sentimento é bastante pronunciado durante as recessões. Durante as expansões o número médio de palavras positivas (normalizado) era de 1,21 versus 2,05 para palavras negativas. Já nas recessões esta relação era de 1,15 versus 2,09. Esta diferença é significativa em termos estatísticos.

Leia mais em GARCIA, Diego. Sentiment during Recessions. Journal of Finance. Vol. LXVIII, n. 3, jun. 2013.

Na área de finanças comportamentais tem-se estudado como os sentidos influenciam as decisões financeiras. Pesquisas já comprovaram que o mercado acionário é influenciado pelo tempo, pelos resultados dos esportes, pela superstição, pelas notícias da imprensa, entre outras situações.

Diego Garcia, um pesquisador da Universidade da Carolina do Norte, resolveu investigar o papel da imprensa e o comportamento do mercado acionário. Para isto, ele usou uma de mais de cinquenta mil artigos que foram publicados diariamente no New York Times e Wall Street Journal, desde 1905 até 2005, sobre o mercado financeiro. Analisando cada um destes textos, Garcia classificou as palavras negativas (irregular, declínio, perda, destruição, etc) e positivas. Ao confrontar a quantidade de palavras de cada um dos grupos, para cada texto analisado, Garcia elaborou um índice de pessimismo do texto. De uma maneira geral, ele encontrou que os textos dos jornais são pessimistas, já que o número de palavras otimistas é menor que as negativas.

Além disto, ele comparou o índice, que representaria uma aproximação do sentimento do mercado ao longo do tempo, com o comportamento do próprio mercado. E encontrou que o sentimento é bastante pronunciado durante as recessões. Durante as expansões o número médio de palavras positivas (normalizado) era de 1,21 versus 2,05 para palavras negativas. Já nas recessões esta relação era de 1,15 versus 2,09. Esta diferença é significativa em termos estatísticos.

Leia mais em GARCIA, Diego. Sentiment during Recessions. Journal of Finance. Vol. LXVIII, n. 3, jun. 2013.

18 setembro 2011

02 junho 2011

Double Dip

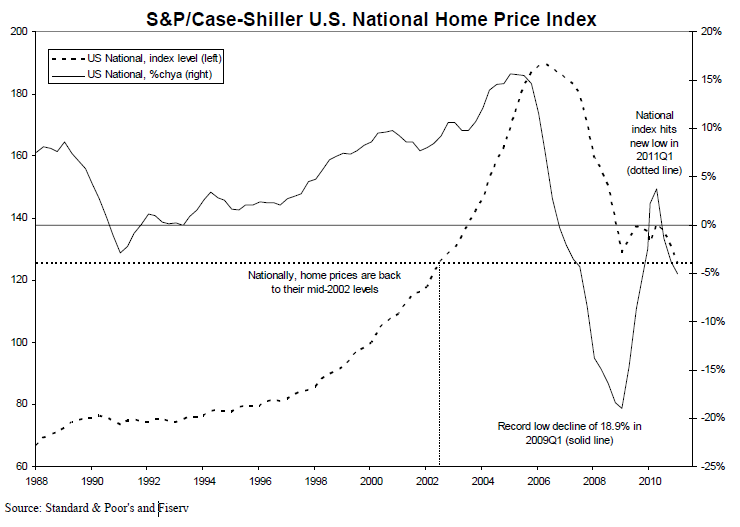

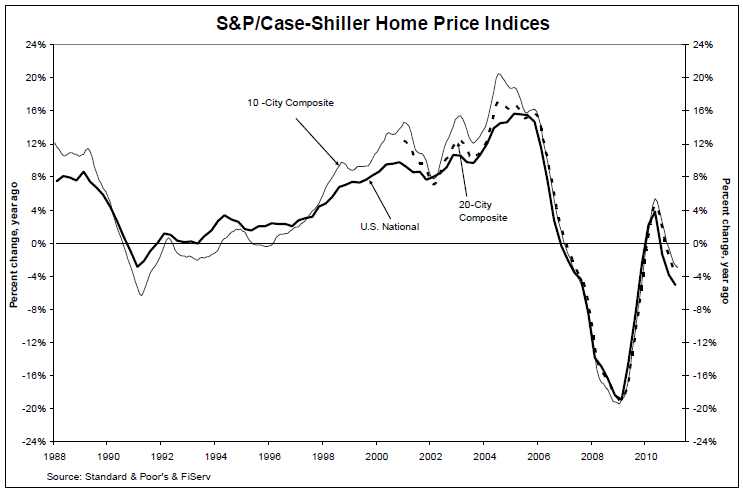

Segunda recessão no mercado imobiliário americano:

“Data through March 2011, released today Case-Shiller Home Price Indices show that the U.S. National Home Price Index declined by 4.2% in the first quarter of 2011, after having fallen 3.6% in the fourth quarter of 2010. The National Index hit a new recession low with the first quarter’s data and posted an annual decline of 5.1% versus the first quarter of 2010. Nationally, home prices are back to their mid-2002 levels.”

Fonte: aqui

“Data through March 2011, released today Case-Shiller Home Price Indices show that the U.S. National Home Price Index declined by 4.2% in the first quarter of 2011, after having fallen 3.6% in the fourth quarter of 2010. The National Index hit a new recession low with the first quarter’s data and posted an annual decline of 5.1% versus the first quarter of 2010. Nationally, home prices are back to their mid-2002 levels.”

Fonte: aqui

04 maio 2009

Recessão e oportunidades

(...) numerosos estudos mostraram que empresas que gastaram em aquisição, propaganda e pesquisa e desenvolvimento durante recessões estavam significativamente melhor do que aquelas que fizeram grandes cortes. (...) As incertezas das recessões criam oportunidades para lucros e existem registros históricos de empresas que fez grandes sucessos em tempos difíceis.

James Surowiecki, Hanging Tough, New Yorker

Assinar:

Postagens (Atom)